By Joshua Stabler – Energy Edge Managing Director

Changes to the Semi-Scheduled Generator Obligations

Increased obligations for Semi-Scheduled and Dispatch Targets

The new rules, due to be implemented on 12 April 2021, will increase the obligation on semi-scheduled generators to meet their AEMO dispatch targets, except for energy resource limitations.

In particular, this means that semi-scheduled generators will have to follow their dispatch targets and are not able to curtail their dispatch during negative prices without a corresponding bid. Given the increasing obligations on rebidding and late rebidding, there is a growing expectation on renewable generators to make active strategic bidding decisions in advance of the trading day.

Third party Legal Reviews

Ashurst was one of the first legal firms to publish a legal review with the following key observations:

- Generators should consider whether any software used to optimise dispatch in response to price remains fit for purpose in light of these new rules. In doing so, they may need to:

- rewrite generator operating procedures;

- brief operating staff; and

- disable any automated systems that enable negative pricing curtailment without rebidding or waiting for an updated dispatch instruction.

- Given the increasing prevalence of negative price periods in the NEM, stakeholders should ensure that their exposure to negative price risk and curtailment (or turn-down) risk under their PPAs is appropriately managed.

- Generators should remain cognisant of their obligations around rebidding under the National Electricity Rules, particularly in respect of rebids that are made during a ‘late rebidding period’ and the additional requirements that would apply.

Ashurst News and Insights: https://www.ashurst.com/en/news-and-insights/legal-updates/new-rules-clarify-dispatch-obligations-for-semi-scheduled-generators-in-australia

Managing Negative Prices as a Renewable Generator

Setting the scene for a renewable generator

Renewable generators are characterized by four important features for our discussion today:

- The cost of fuel is effectively zero. Solar and Wind energy resources are produced without cost and without precise control.

- Due to the value of Large-scale Generation Certificates (LGCs), which are produced by Renewable generators based on energy dispatched at node, it is standard practice for the assets to dispatch at a negative marginal price.

- It is not unusual for Renewable assets to have power purchase agreements (PPA) in place to help with the financing of the asset. It is also generally accepted that the PPA will have an embedded zero-strike floor option, which places the financial exposure of negative prices on the asset operator, not the PPA purchaser.

- Generation assets are attracted to similar locations due to the availability of renewable resources, which has been noted with the wind assets located in South Australia, Victoria and Tasmania, which are fueled by similar meteorological conditions. This means that common transmission networks can be impacted by congestion. None of these high renewable resource locations are co-located with the existing regional reference nodes.

Realistic Market Scenarios

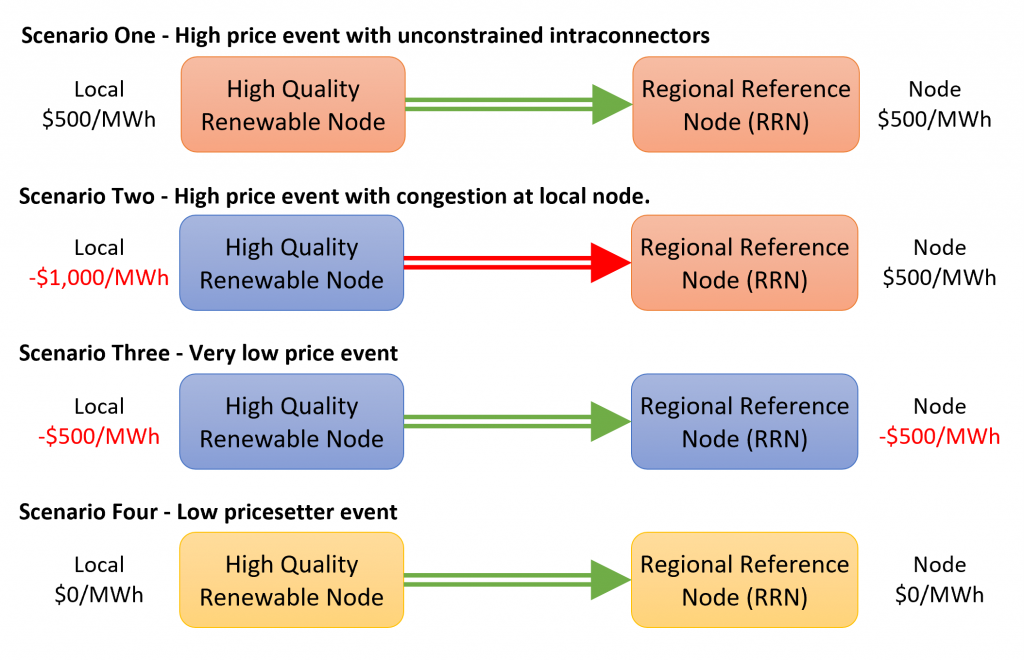

Let’s look at four common scenarios in the electricity market that a renewable generator will need to consider (see Figure 1).

Figure 1 – Managing four market scenarios including network constraints and different local and nodal market prices

Scenario Response

Scenario One – High (or normal) price event with unconstrained interconnectors.

This is our most common scenario. The market is operating normally. There are no constraints and the market price is within its normal range.

Under these conditions, renewable generators with negative marginal costs (very low on the merit order) are highly motivated to dispatch at full capacity. However, the exact price bands (either at either the negative marginal cost or market floor) of the generator offer for dispatch will have limited direct impact on the cleared dispatch volume and settled price by the AEMO NEMDE (Market operator’s National Electricity Market Dispatch Engine).

Therefore, Generator Offers at marginal cost (say -$30/MWh), at market floor (-$1000/MWh) or at $0/MWh will also have similar financial outcomes.

Scenario Two – High price event with congestion at local node

Under the circumstances where there are network constraints which limit the ability for the energy from local generators to reach the regional reference node, a local generator is motivated to offer their dispatch at the market floor price (-$1,000/MWh) in order to maximise their dispatch.

That is, if the shadow price for the region is -$1000/MWh, any assets with offers at their fuel cost (-$30/MWh) will be targeted to zero dispatch. The remaining assts that offered their volume at the market floor price floor will be dispatched subject to the price breaker rules (i.e. pro-rata dispatch).

So for the same price conditions at the node for Scenario One and Scenario Two, we see different bidding behaviour strategies.

Scenario Three – Very low price event

Under the circumstance where both the local and regional reference node prices are substantially negative, the motivations of the generators will change. If the renewable asset has market exposure to negative prices (due to negative embedded floor or due to spot exposure), the asset is motivated to limit their dispatch to avoid the real cost of the energy market (i.e. paying to generate).

Therefore, if a generator has offered their energy at their fuel cost, they will be scheduled offline. Whereas any generators that offered their dispatch at the market floor price will be still receiving dispatch targets as well as the newly minted obligation (as of 12 April 2021) to dispatch to meet those targets.

We have now split the operational behaviour of the renewable generators between competing for dispatch during local negative market prices based on the regional reference price and the misalignment between the two regions.

Scenario Four – Low price setter event

The scenario four conditions provide an alternative scenario, which is dependent on the pool exposure of the individual participants. If the market price is being set by the generator assets at their marginal cost (i.e. -$30/MWh), there is a potential volume / price trade-off that could be considered.

Under this hypothetical scenario, it is potentially possible for the generator to withdraw some of their dispatch capacity and place it at a higher price band, potentially causing the market price to rise (potentially from not at all to substantially) and, therefore, potentially increase the pool gross margin for the business.

This type of behaviour has been historically exercised by large incumbent businesses where the pool exposures and power station volume have been more substantial, and the gross margin pay-off between lost pool exposure and higher gross margin revenue is considerable.

Responding to the market signals

One of the major complexities of the four scenarios is the ability to forecast the market conditions and decide the appropriate trading strategy to incorporate in advance of the conditions and having the confidence that your bidding behaviour is appropriate in a five minute market.

Energy Edge Electricity Forecasting Service (EFS)

Energy Edge have developed the Electricity Forecasting Service (EFS) which provides a seven-day ahead spot price forecast for each region based on key methodology assumptions defined by the client.

Rather than the deterministic bottom-up modelling systems which require a declaration of the capacity of complex power stations on a unit-by-unit basis, the EFS uses a market generalization with a top-down approach based on a definable training period for the forecast outcomes.

Short Term: Seven Day Forecast

The EFS has an automated daily forecast for the next seven-days sent to your email inbox each morning which incorporates updates to the Short Term Projected Assessment of System Adequacy (STPASA) availability, demand and market conditions.

Using the forecast spot prices, renewable generators will be able to anticipate the market conditions and which of the above market scenarios that the business needs to manage. The Short Term EFS is currently available for client subscription right now (Electricity Forecasting Service).

Medium Term and Long Term Forecast

Energy Edge is in the process of transferring the core methodology of its medium-term and long-term forecast and data controls into the same automatic systemic functionality as the short term forecast.

The Medium Term Forecast will incorporate the recent extension of the Medium Term Projected Assessment of System Adequacy (MTPASA) to a three-year horizon, whereas the Long Term Forecast will incorporate the macro assumptions like investment cycles. The Medium Term EFS and Long Term EFS will be available to clients during late 2021.

What can you do next?

Contact Us to find out more about our electricity forecasting service and how it can help you make confident decisions in the electricity market ahead of time.