The risk and analytics component of Market Edge enables participants to input a range of factors including forecasts of production and load, fuel supply and financial products to formulate an appropriate strategy. It also produces a wide variety of risk and analytics reporting capability that can be tailored to a client’s requirements.

Key functions include:

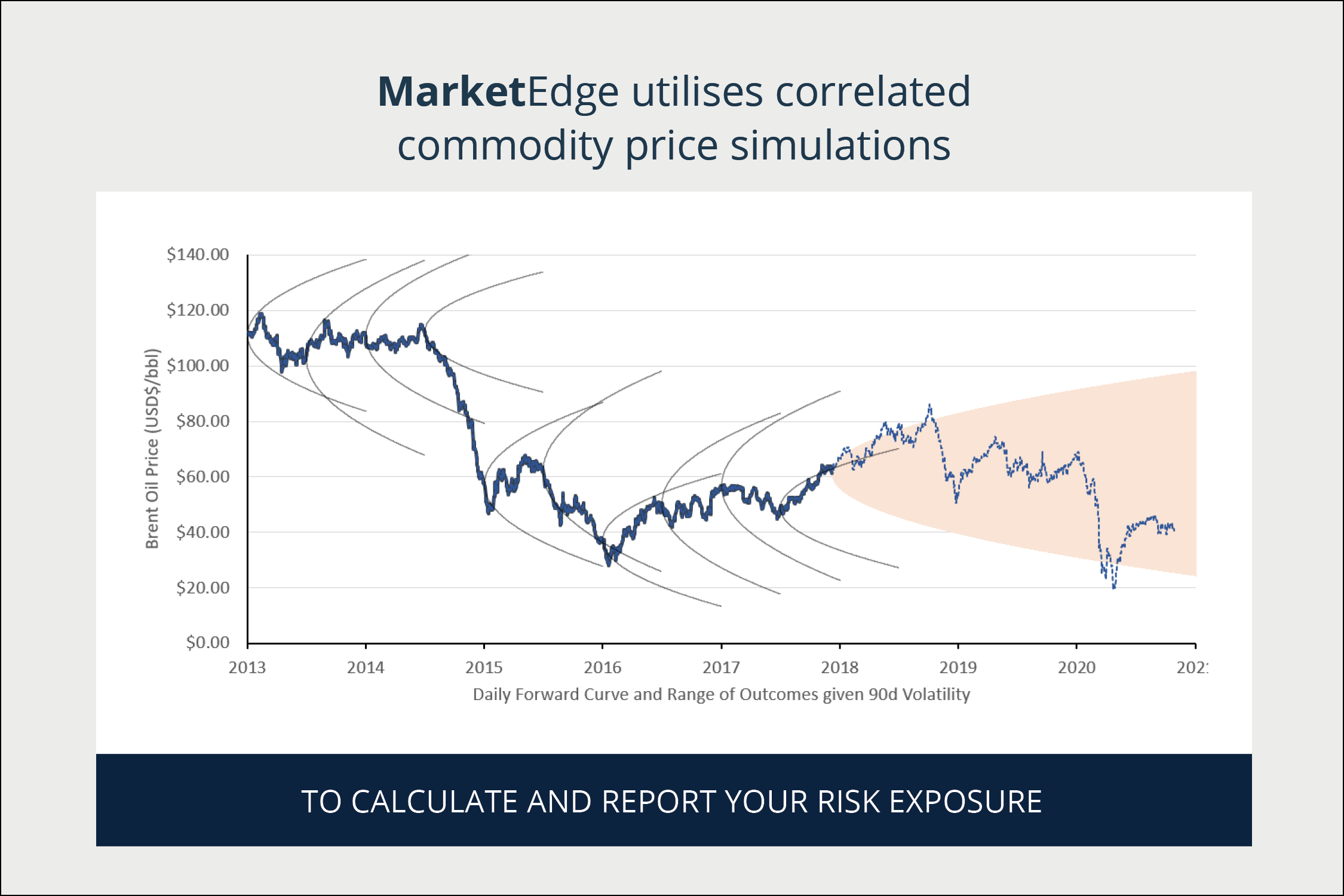

- Multi-Commodity Simulations – Integration of correlation matrix for simulations of forward and physical market conditions

- Pricing Tools – Transfer and fair value pricing calculations of derivative contracts

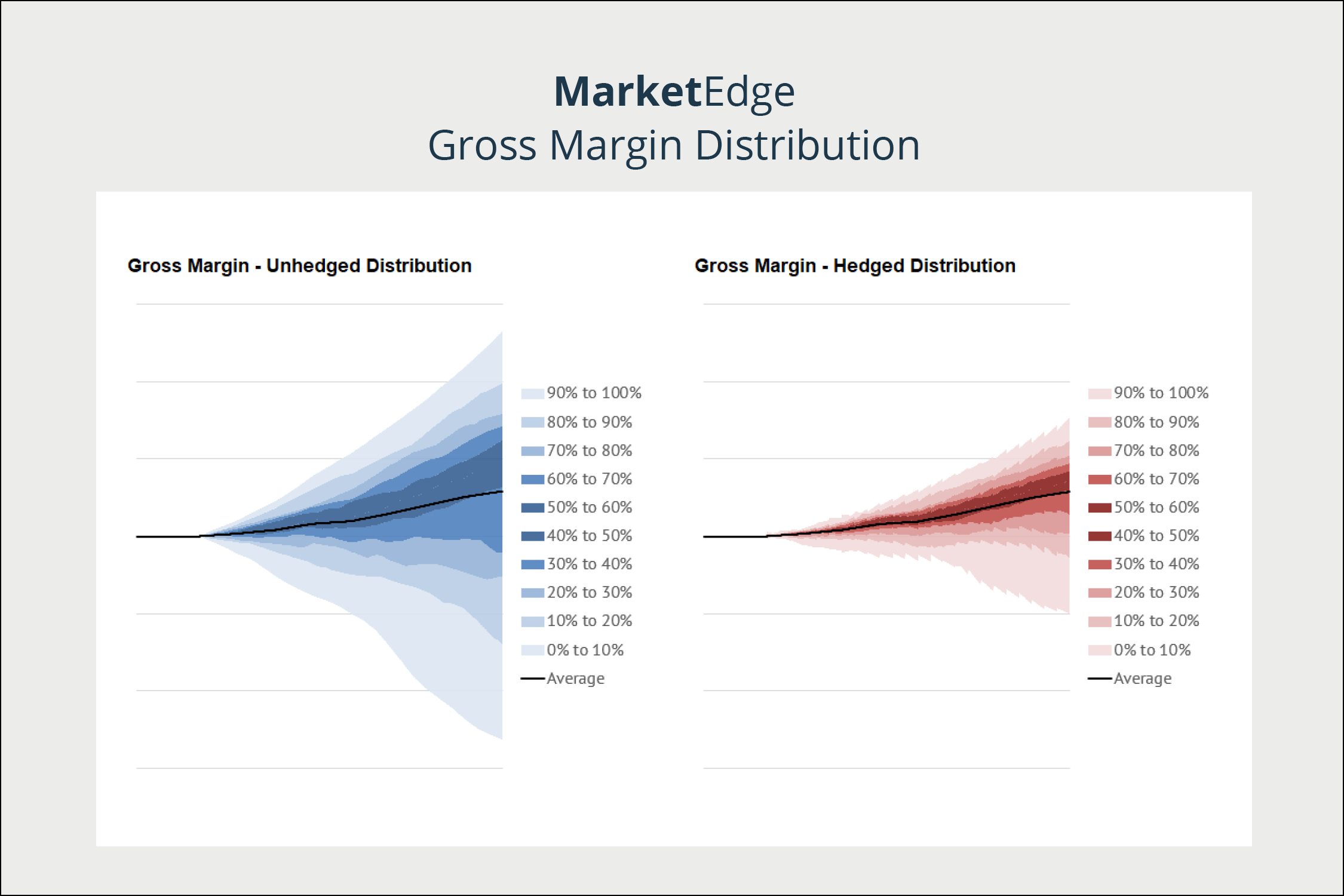

- Portfolio Optimisation – Calculation of market volume, price and credit risk and the development of optimal (minimum risk) hedging portfolio strategies including physical portfolio dispatch methodologies

- Inventory Management – Environmental certificates and other registries

- Credit Risk Tools – Mark to market, settlement calculations and invoicing, counterparty credit (total & residual exposure and at-risk) and credit support arrangement calculations

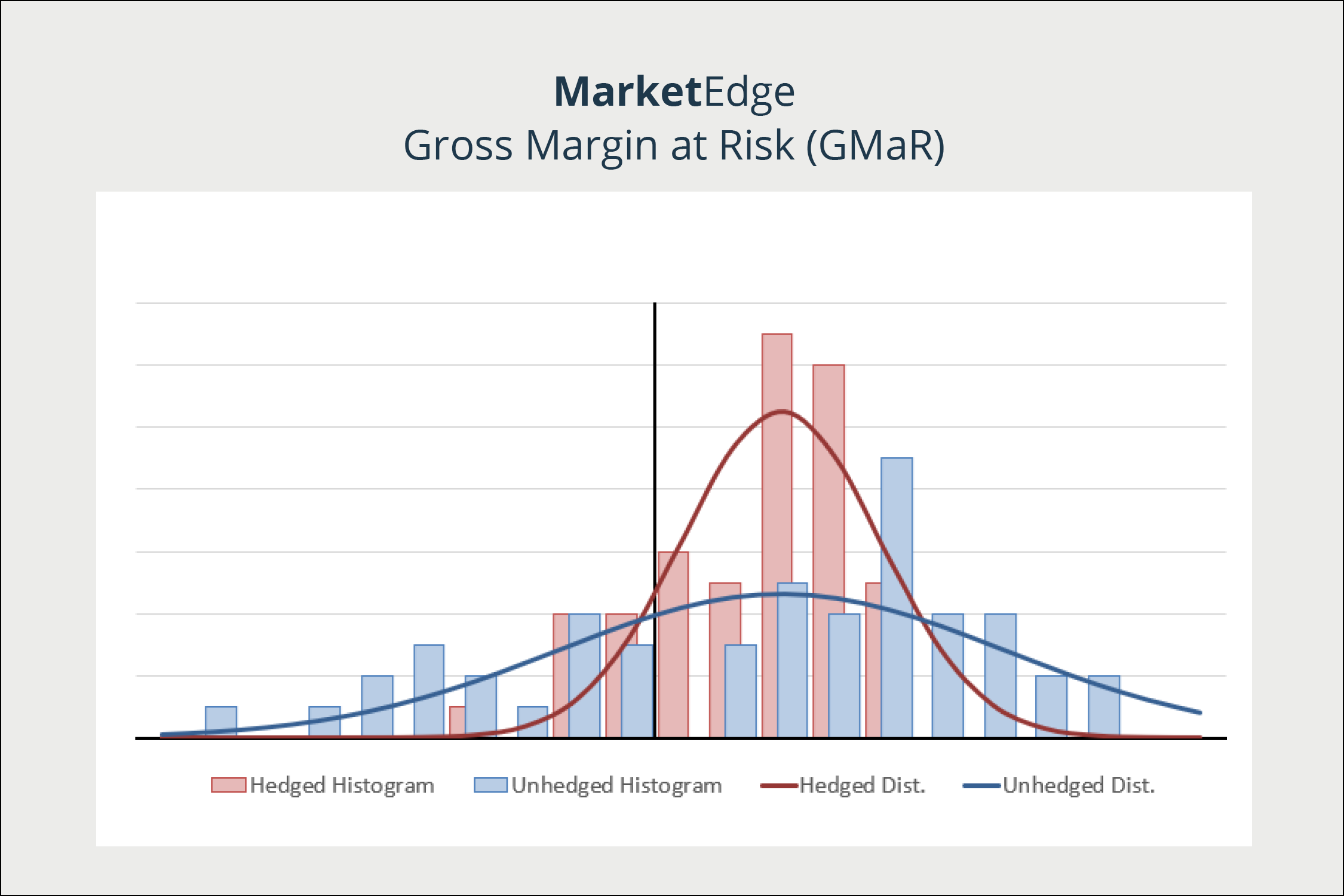

- Portfolio Risk Reporting – Gross Margin at Risk (GMaR), Earnings at Risk (EaR), Value at Risk (VaR), Cash Flow at Risk (CFaR), Futures Margins at Risk (FMaR)

- Add Hedge Effectiveness Testing to Market Edge – Accounting treatment of hedge effectiveness testing